Where do I invest my small amounts of money I am saving?

For young adults this couldn't be a better time. The market is low and you have time. All you have to do is ACT! What are you waiting for? T Rowe Price has an account you can start for $50 a month or $1000. If you go with the automatic account builder it will help you make small changes so you can continue to contribute every month. We are talking $12.50 a week. One less fast food meal and speciality coffee a week - will start to build you wealth and security.

Basic Rules for Investing in an IRA

1 Need earned income

2. 2009 limit $5000, if over age 50 $6000

3. Can not contribute more that you earn

4. Roth IRA is normally the best choice for young investors

6. Investment - research all in one funds/target retirement date

T. Rowe Price gives an excellent data sheet on the differences and eligibility for IRA investing. If you have concerns feel free to comment on the blog and I will be happy to answer your questions. After much research T Rowe Price had the lowest minimum to get a new investor started. Other discount firms such as Fidelity Investments had a minimum of $200 amount on an automatic account builder and Vanguard had a $3000 minimum.

As always check with a financial professional before making an investment decisions. All the above companies have licensed representatives available to answer your questions and assist you. They are all salaried and not on commission. This keeps fees low and the representative from pressuring you into a product you don't need. As always check with a financial professional prior to making any investment decisions. Happy Investing...

Stay tuned................

29 April 2009

26 April 2009

Question about Saving - Back to Basics of GenM

Comment from article about my uncle and not having money in retirement.

Where are you supposed to save those small amounts? can you fully trust banks?also, if the amounts are small now, they will be worthless in the future... unless you save lots and lots of small amounts....

GenM - Time is on your side -So what is one of the pieces of the puzzle? "Time + Regular Investing" into a diversified portfolio = Long term success.

The sooner you start investing in a 401k or IRA the more $$ you have for retirement.

If you invest $60 a week or $8.56 a day starting at age 18 for 50 years with an 8% return = $1.9 Million.

If you invest $60 a week starting at age 25 for 42 years with an 8% return = $1 Million

By waiting 7 years to invest a mere $60 a week - you give up almost one million dollars.

Where am I going to get $60 a week ??..... it is so easy with simple changes you won"t notice in the long run........Pack your lunch instead of eating out - Go to the library for movies, cds, books and games - Plan your route to avoid extra driving - Go to a matinee - Drink water vs ordering soda, coffee, tea etc. Clip coupons. Most cities offer free events - check local newspaper. Little changes that will not affect your quality of life TODAY will pay off big TOMORROW. This information can change your entire generation - WILL YOU BE A MILLIONAIRE?

Where are you supposed to save those small amounts? can you fully trust banks?also, if the amounts are small now, they will be worthless in the future... unless you save lots and lots of small amounts....

GenM - Time is on your side -So what is one of the pieces of the puzzle? "Time + Regular Investing" into a diversified portfolio = Long term success.

The sooner you start investing in a 401k or IRA the more $$ you have for retirement.

If you invest $60 a week or $8.56 a day starting at age 18 for 50 years with an 8% return = $1.9 Million.

If you invest $60 a week starting at age 25 for 42 years with an 8% return = $1 Million

By waiting 7 years to invest a mere $60 a week - you give up almost one million dollars.

Where am I going to get $60 a week ??..... it is so easy with simple changes you won"t notice in the long run........Pack your lunch instead of eating out - Go to the library for movies, cds, books and games - Plan your route to avoid extra driving - Go to a matinee - Drink water vs ordering soda, coffee, tea etc. Clip coupons. Most cities offer free events - check local newspaper. Little changes that will not affect your quality of life TODAY will pay off big TOMORROW. This information can change your entire generation - WILL YOU BE A MILLIONAIRE?

Next post will be where to invest the small amounts of money....

Stay tuned.......

23 April 2009

Mint.com - Aaron Patzer

I have been using http://www.mint.com for months and have posted about the genius of this website numerous times. Mint is a financial tracking website that has simplified the process of tracking your money, expenses, budget and actually makes recommendations on ways to save money or earn more money - by offering products that may better suit your needs. Mint is free to users.

I had the pleasure to meet Aaron last night at the Greater Cincinnati Venture Association meeting and he is as impressive in person as he is in his work. He was the Keynote speaker and talked about the commitment to being an entrepreneur. He discussed his failures prior to Mint and the steps taken to get Mint to the point of being a product that he could present to potential backers.

If looking to start your own business - here were a few of Aaron's thoughts.

1. You don't have a social life, he locked himself in a room for 14 hours a day for over a year to create a product he could bring to the table. He used his own money and quit his job to focus on Mint.com

2. The most important part of any business, product, or invention is that it must solve a real need and a real problem. Observe the world around you – everything you do, and especially everything you hate to do – solve a real problem and the world is yours.

3. Sit alone for an hour or two each week, no distractions and think about your business and product. Hard thinking is easy to avoid.

4. Prior to launch-to build buzz was start a very active blog with over 200 articles on personal finance. To get into the Mint.com private beta first, you needed to put up a little badge on your blog or social network page that said “I want Mint!”. That gave us lots of free advertising, and a ton of inbound links which improved our ranking in Google – not only was it free, it made those customers feel special when we let them in early.

Mint is approaching 2 million users and continuing to improve the site that was already excellent.

Stay tuned......

I had the pleasure to meet Aaron last night at the Greater Cincinnati Venture Association meeting and he is as impressive in person as he is in his work. He was the Keynote speaker and talked about the commitment to being an entrepreneur. He discussed his failures prior to Mint and the steps taken to get Mint to the point of being a product that he could present to potential backers.

If looking to start your own business - here were a few of Aaron's thoughts.

1. You don't have a social life, he locked himself in a room for 14 hours a day for over a year to create a product he could bring to the table. He used his own money and quit his job to focus on Mint.com

2. The most important part of any business, product, or invention is that it must solve a real need and a real problem. Observe the world around you – everything you do, and especially everything you hate to do – solve a real problem and the world is yours.

3. Sit alone for an hour or two each week, no distractions and think about your business and product. Hard thinking is easy to avoid.

4. Prior to launch-to build buzz was start a very active blog with over 200 articles on personal finance. To get into the Mint.com private beta first, you needed to put up a little badge on your blog or social network page that said “I want Mint!”. That gave us lots of free advertising, and a ton of inbound links which improved our ranking in Google – not only was it free, it made those customers feel special when we let them in early.

Mint is approaching 2 million users and continuing to improve the site that was already excellent.

Stay tuned......

22 April 2009

Earth Day!

I love the universe - this has been my mantra for the past 14 years.

Before that I honestly never thought about it. I am part of a generation that believed litter was bad, fought to clean up the factories. (I lived near a Steel Plant - we would literally have a coating of black soot on our cars every morning) and wanted the water clean. It was more single focused we missed the bigger picture. We never dreamed the Artic shelf could melt or break apart, glaciers would fade into the water, rainforest's would be depleted and animals would become extinct.

So what changed 14 years ago that I became aware of the sanctity of the Universe. Exposure. I was fortunate enough to be able to start to travel to other parts of the world. When you come face to face with an animal that may be extinct due to our selfishness and ignorance - it changes you. While I watched the glaciers calving and splashing into the water - I felt a sense of awe and sadness. When I saw people walking miles for water because their natural supply either dried up or is polluted - it changes you and how you view all the privileges we live with everyday.

If you are not able to travel I urge you to watch the series PLANET EARTH. Open your mind and heart and see all the amazing facets of our universe. It will change you.

There are tips all over the internet on steps you can take to go GREEN - but if you don't have a true shift in your thinking and beliefs - you won't act on them. Take a day, make some popcorn, and relax and embrace the amazing PLANET EARTH - then take little steps to change your actions - you can make a difference!

Stay tuned........

20 April 2009

On the Road to Riches

Let's look at someone who is on the right track..... Our guest blogger Stefan has agreed to let us track his success over time. He called me very excited last week as his networth went over $10,000.

He is 23 years old and a recent graduate of Ohio State University.

First job starting salary $35,000 a year.

First annual review - amazing and was promoted to next level and given a performance bonus.

No debt other than student loans that he is paying off ahead of schedule.

Between his 401k, Roth IRA and Emergency savings he has over 10K.

He increased his 401k contribution from 15% to 16% when he received his bonus.

He continues adding $100 a paycheck to his emergency savings - and is considering increasing.

He is currently educating himself on real estate so when the right deal comes along he is ready to make a decision.

It goes to show you do not have to make alot of money to slowly increase your financial security. Everyday choices and being aware of how you spend your money - makes the difference.

We will check in with Stefan on a quarterly basis to see how he is progressing.

Stay tuned...

17 April 2009

Live for Today - End Up Broke Later.......

I have made it home from my journey to Florida to save my Uncle from his eventual demise and helped my mother not go into a depression over the whole situation.

As promised - the story of the people we bought the trailer condo from.

A very nice couple in their early sixties in a panic to sell their home. They thought they did everything right. Worked hard, saved in their 401k's, raised their children and bought a retirement place to spend the winters at.

A few things happen to them. First, the home they purchased up north was very expensive. It was a home on a lake that feed into a river. They thought having water property they could never lose. However, due to commerce - and a natural disaster a decade ago - the lake literally dried up and has never been able to replenish itself.

The property was now worth way less than they owed on it. So they are trapped in this situation. On top of it the housing market has plummeted which made the situation worse.

When they bought their trailer in Florida they bought on the high side. They retired to early and the stock market dropped significantly. They can not make their payments and their dreams of living out retirement in ease - turned to disaster.

The bottom line is - financial planning never ends. If planning to live on your savings - you have to have it invested appropriately so you don't lose it if the economy goes bad.

The main message again is - if you start saving small amounts of money NOW over the long term - you may be able to avoid being in these types of situations.

Stay tuned......

As promised - the story of the people we bought the trailer condo from.

A very nice couple in their early sixties in a panic to sell their home. They thought they did everything right. Worked hard, saved in their 401k's, raised their children and bought a retirement place to spend the winters at.

A few things happen to them. First, the home they purchased up north was very expensive. It was a home on a lake that feed into a river. They thought having water property they could never lose. However, due to commerce - and a natural disaster a decade ago - the lake literally dried up and has never been able to replenish itself.

The property was now worth way less than they owed on it. So they are trapped in this situation. On top of it the housing market has plummeted which made the situation worse.

When they bought their trailer in Florida they bought on the high side. They retired to early and the stock market dropped significantly. They can not make their payments and their dreams of living out retirement in ease - turned to disaster.

The bottom line is - financial planning never ends. If planning to live on your savings - you have to have it invested appropriately so you don't lose it if the economy goes bad.

The main message again is - if you start saving small amounts of money NOW over the long term - you may be able to avoid being in these types of situations.

Stay tuned......

15 April 2009

Live for Today ... What Really Happens.....

I have had the most stressful week of my life...... This is what happens when people do not plan and live for only today.

My Uncle has been taken care of by my family for 67 years. He never had any responsibility while growing up - my grandparents spoiled him beyond belief. He then got married young, had 3 children and had to go to Vietnam for 2 terms. When he came back - he was out of control - his wife left him and my grandparents continued taking care of him. My grandmother died of cancer in 1986 and was still doing his laundry. He moved in with my grandfather and still lives in that house. We moved my grandfather back to Ohio in 1998 and since my Uncle had nothing - they left him in that house. My mom and her sister have basically paid his way until today.

He has had part time jobs and makes alittle here and there, He basically barters for most of his belongings and lives very simply. However, he has the continual fear of what is going to happen to him. When something would happen to my Aunt or mother - he will be out on the street. As my siblings have opted to not carry this to a third generation.

This last week I have spent with my mom, sister and cousin trying to figure out how to change this situation. We all have the same goal in mind - security for my uncle and freedom for all of us. We are a very close family and this could have easily turned into a feud. The amount of stress that comes with money issues is unbelievable. Then tie in emotions and everyone's thoughts .... it is a disaster in the making.

Fortunately, we found a solution. There is something called a Condo Trailer Park in Florida. You actually own the land and put a trailer on it. They are very nice. We were able to find an affordable one for him and he was willing to move. He now has security as long as he pays his Condo dues and taxes. We are free from worrying about what will happen to him and my parents can now enjoy the house, rent it or sell it.

My uncle is very fortunate that people cared about him. Most people in this situation would have been homeless a long time ago. This is an extreme example however, had he made a few different decisions his life could have been very different.

Next blog is going to be on the people we bought the trailer from and their financial woes......

Freedom - plan for your life. Small amounts of money over a long time can equal freedom and options.

Stay tuned......

My Uncle has been taken care of by my family for 67 years. He never had any responsibility while growing up - my grandparents spoiled him beyond belief. He then got married young, had 3 children and had to go to Vietnam for 2 terms. When he came back - he was out of control - his wife left him and my grandparents continued taking care of him. My grandmother died of cancer in 1986 and was still doing his laundry. He moved in with my grandfather and still lives in that house. We moved my grandfather back to Ohio in 1998 and since my Uncle had nothing - they left him in that house. My mom and her sister have basically paid his way until today.

He has had part time jobs and makes alittle here and there, He basically barters for most of his belongings and lives very simply. However, he has the continual fear of what is going to happen to him. When something would happen to my Aunt or mother - he will be out on the street. As my siblings have opted to not carry this to a third generation.

This last week I have spent with my mom, sister and cousin trying to figure out how to change this situation. We all have the same goal in mind - security for my uncle and freedom for all of us. We are a very close family and this could have easily turned into a feud. The amount of stress that comes with money issues is unbelievable. Then tie in emotions and everyone's thoughts .... it is a disaster in the making.

Fortunately, we found a solution. There is something called a Condo Trailer Park in Florida. You actually own the land and put a trailer on it. They are very nice. We were able to find an affordable one for him and he was willing to move. He now has security as long as he pays his Condo dues and taxes. We are free from worrying about what will happen to him and my parents can now enjoy the house, rent it or sell it.

My uncle is very fortunate that people cared about him. Most people in this situation would have been homeless a long time ago. This is an extreme example however, had he made a few different decisions his life could have been very different.

Next blog is going to be on the people we bought the trailer from and their financial woes......

Freedom - plan for your life. Small amounts of money over a long time can equal freedom and options.

Stay tuned......

10 April 2009

Flip Flops or a Beach House??

Flip flops or a beach house -- what will it be?? When I was at a recent convention I found it fascinating that I was giving away alot of money - all it took was 1 minute of time to give a guess. However, there was a novelty booth directly across from me - and they had the allure of decorating flip flops. It was like gnats to a fire.........

So my question to all of you is -- what do you really want? Instant gratification and the flash and color of something new that will last a few weeks or a beach house that you can relax in for years and years, as well as, security and piece of mind???

That experience was a microcosm of what life is really like and unless you make a conscious decision to go for the big stuff and give up the flashy fun stuff that does not change your life - you will always be chasing the flame and never getting to the reward - you will continually get burned.

Stay tuned....

So my question to all of you is -- what do you really want? Instant gratification and the flash and color of something new that will last a few weeks or a beach house that you can relax in for years and years, as well as, security and piece of mind???

That experience was a microcosm of what life is really like and unless you make a conscious decision to go for the big stuff and give up the flashy fun stuff that does not change your life - you will always be chasing the flame and never getting to the reward - you will continually get burned.

Stay tuned....

08 April 2009

Advice Men vs. Women.....

Interesting article from Nina..

Investment advice comes in all shapes and sizes. Grab a few back issues of Esquire and a quick scan of its “investing” columns reveals “investing” advice. For example, they give opinions on buying Wal-Mart, selling Apple, and buying the Baby Bells vs. Cable Companies.

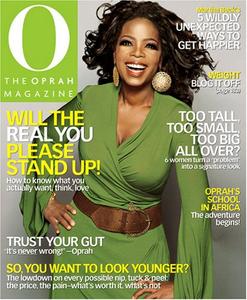

But do the same with O, the Oprah Magazine and this is what the editors categorize as “investing”:

How to buy life insurance

The basics of financial planning and investing

Home finance basics everyone should know

Know how much home you can afford

How to play rollover with your 401(k)

So here’s my Aha! moment: why do men get “investing” advice in their magazines and we get financial basics in ours?

Women get touchy-feely encouragement Suze Orman is an O Magazine columnist and typically I like her advice. She’s spot on when it comes to buying a used car and term life insurance. But when speaking to women, is she talking down to us?

Case in point: look at what she says about establishing a rainy day fund in this O article. She writes, “Ideally, you will have eight months of living expenses stashed in a savings account. I know that sounds daunting, but make it a goal. Start putting away a little each month. Every penny you save is a step toward building your own personal insurance plan.”

Ahem… “I know that sounds daunting but make it a goal.”

Would a male personal finance expert ever instruct a man this way?

Men get hard-hitting advice Ken Kurson, the columnist at Esquire and author of The Green Magazine Guide to Personal Finance: A No B.S. Money Book for Your Twenties and Thirties writes, “You’re keeping your emergency cash in a money market fund. In other words, don’t fund the expansion of your portfolio into stocks and bonds with the money you’re keeping on reserve, but feel free to consider that money part of your portfolio.”

See the difference? First let’s consider the demographics of O Magazine: The median age is 45, readership is predictably female (91%), married (66%), and a median household income of $88,000. Their readers aren’t exactly females fresh out of college.

So Orman is encouraging forty year old women to make sure they have an emergency fund and Kurson assumes twentysomething guys already have a stash in reserve. Perhaps this is why CNBC gets Jim Cramer and The Today Show has Jean Chatzky.

A commenter at BloggingStocks had this analysis of Orman’s writings by saying, “When someone is talking to me about money, I want math. I bought one of Suze’s books and when she started talking about how I ‘felt’ about my money, I put the book down in disgust. Behavior patterns as applied to money fall under psychology; everything else is quantifiable. I don’t need to have a good relationship with my money; I need to understand how the stock market, the housing market and my 401K work.”

Gender-specific behaviors with moneyBut do female money experts talk down to us or are we inviting the tone by behavior? After all, according to Manisha Thakor and Sharon Kedar, authors of On My Own Two Feet, the average woman between ages 24 and 35 has only $500 in savings.

Woman’s Day acts like their readers only have $500 in savings as well and I don’t know any women under fifty subscribing to that magazine. Mary Hunt is their columnist and a quick glance at her 2007 columns reveal topics like “Big Online Bargains” and “Slash Your Food Bills”.

Kay Bell, the blogger at Don’t Mess with Taxes, gives her perception on the male vs. female financial behaviors. She writes, “Even today, some gender-specific societal expectations manage to persist… That is, a lot of women take a more ‘supportive’ fiscal approach, focusing on money maintenance, holding on to what they have, instead of taking steps to advance it.”

“We need to get over that right now and get more aggressive when it comes to money – making it, saving it, investing it. The go-for-it approach seems to be more typical of male financial bloggers. Men, at least in my anecdotal observations, are more apt to be risk takers with their money. They embrace the idea that to make more money you sometimes have to take some financial risks with what you’ve got.”

And it’s not just OprahI couldn’t find any money advice in InStyle magazine, but they offer plenty of ideas on how to spend it. Glamour claims to have a money expert, but the only thing I could find was an online debt quiz. Take it and see how you stack up with their readers. If you’re a regular follower of personal finance blogs then it’s likely you’re way of ahead of these well-heeled and in style consumers.

Just to be fair and balanced, I reviewed some other men’s magazines and money was either missing or sexualized and presented by young, attractive female writers. Check out the article by Anya Kamenetz in Men’s Health called, 7 Financial Habits of Highly Laid Men. Enough said – otherwise this might segue into a different discussion.

But maybe money is missing from general interest magazines because men go to the source for their financial advice by subscribing to the money periodicals. As an example here is the male / female readership break down for Fortune and Money:

Money: Male/Female (64% / 36%)Fortune: Male/Female (79% / 21%)

And guess who is reading The Wall Street Journal and Financial Times?

Money spends the same whether it’s carried in a purse or walletSo does tone and depth of the advice really matter? In the end, money is money and basic truths are better than nothing at all. But if empowerment and financial independence are what Suze Orman wants for the ladies, then maybe it’s time to butch up the advice. Don’t sugarcoat or wrap it in a soft, pretty package. We’re ready to take it like a man! That’s how you turn women savers into women investors!

Finally, for the sake of starting a conversation below, do you agree that women get fed the softer side of money from women’s magazines? Or will some of you accuse me of gender-generalizing? If you agree, then what should we do about it? Write to Oprah? Or just subscribe to Fortune and Money like the big boys?

—————Nina blogs about money at Queercents.

Stay Tuned

Investment advice comes in all shapes and sizes. Grab a few back issues of Esquire and a quick scan of its “investing” columns reveals “investing” advice. For example, they give opinions on buying Wal-Mart, selling Apple, and buying the Baby Bells vs. Cable Companies.

But do the same with O, the Oprah Magazine and this is what the editors categorize as “investing”:

How to buy life insurance

The basics of financial planning and investing

Home finance basics everyone should know

Know how much home you can afford

How to play rollover with your 401(k)

So here’s my Aha! moment: why do men get “investing” advice in their magazines and we get financial basics in ours?

Women get touchy-feely encouragement Suze Orman is an O Magazine columnist and typically I like her advice. She’s spot on when it comes to buying a used car and term life insurance. But when speaking to women, is she talking down to us?

Case in point: look at what she says about establishing a rainy day fund in this O article. She writes, “Ideally, you will have eight months of living expenses stashed in a savings account. I know that sounds daunting, but make it a goal. Start putting away a little each month. Every penny you save is a step toward building your own personal insurance plan.”

Ahem… “I know that sounds daunting but make it a goal.”

Would a male personal finance expert ever instruct a man this way?

Men get hard-hitting advice Ken Kurson, the columnist at Esquire and author of The Green Magazine Guide to Personal Finance: A No B.S. Money Book for Your Twenties and Thirties writes, “You’re keeping your emergency cash in a money market fund. In other words, don’t fund the expansion of your portfolio into stocks and bonds with the money you’re keeping on reserve, but feel free to consider that money part of your portfolio.”

See the difference? First let’s consider the demographics of O Magazine: The median age is 45, readership is predictably female (91%), married (66%), and a median household income of $88,000. Their readers aren’t exactly females fresh out of college.

So Orman is encouraging forty year old women to make sure they have an emergency fund and Kurson assumes twentysomething guys already have a stash in reserve. Perhaps this is why CNBC gets Jim Cramer and The Today Show has Jean Chatzky.

A commenter at BloggingStocks had this analysis of Orman’s writings by saying, “When someone is talking to me about money, I want math. I bought one of Suze’s books and when she started talking about how I ‘felt’ about my money, I put the book down in disgust. Behavior patterns as applied to money fall under psychology; everything else is quantifiable. I don’t need to have a good relationship with my money; I need to understand how the stock market, the housing market and my 401K work.”

Gender-specific behaviors with moneyBut do female money experts talk down to us or are we inviting the tone by behavior? After all, according to Manisha Thakor and Sharon Kedar, authors of On My Own Two Feet, the average woman between ages 24 and 35 has only $500 in savings.

Woman’s Day acts like their readers only have $500 in savings as well and I don’t know any women under fifty subscribing to that magazine. Mary Hunt is their columnist and a quick glance at her 2007 columns reveal topics like “Big Online Bargains” and “Slash Your Food Bills”.

Kay Bell, the blogger at Don’t Mess with Taxes, gives her perception on the male vs. female financial behaviors. She writes, “Even today, some gender-specific societal expectations manage to persist… That is, a lot of women take a more ‘supportive’ fiscal approach, focusing on money maintenance, holding on to what they have, instead of taking steps to advance it.”

“We need to get over that right now and get more aggressive when it comes to money – making it, saving it, investing it. The go-for-it approach seems to be more typical of male financial bloggers. Men, at least in my anecdotal observations, are more apt to be risk takers with their money. They embrace the idea that to make more money you sometimes have to take some financial risks with what you’ve got.”

And it’s not just OprahI couldn’t find any money advice in InStyle magazine, but they offer plenty of ideas on how to spend it. Glamour claims to have a money expert, but the only thing I could find was an online debt quiz. Take it and see how you stack up with their readers. If you’re a regular follower of personal finance blogs then it’s likely you’re way of ahead of these well-heeled and in style consumers.

Just to be fair and balanced, I reviewed some other men’s magazines and money was either missing or sexualized and presented by young, attractive female writers. Check out the article by Anya Kamenetz in Men’s Health called, 7 Financial Habits of Highly Laid Men. Enough said – otherwise this might segue into a different discussion.

But maybe money is missing from general interest magazines because men go to the source for their financial advice by subscribing to the money periodicals. As an example here is the male / female readership break down for Fortune and Money:

Money: Male/Female (64% / 36%)Fortune: Male/Female (79% / 21%)

And guess who is reading The Wall Street Journal and Financial Times?

Money spends the same whether it’s carried in a purse or walletSo does tone and depth of the advice really matter? In the end, money is money and basic truths are better than nothing at all. But if empowerment and financial independence are what Suze Orman wants for the ladies, then maybe it’s time to butch up the advice. Don’t sugarcoat or wrap it in a soft, pretty package. We’re ready to take it like a man! That’s how you turn women savers into women investors!

Finally, for the sake of starting a conversation below, do you agree that women get fed the softer side of money from women’s magazines? Or will some of you accuse me of gender-generalizing? If you agree, then what should we do about it? Write to Oprah? Or just subscribe to Fortune and Money like the big boys?

—————Nina blogs about money at Queercents.

Stay Tuned

03 April 2009

What A Deal!

I have a friend who is an amazing couponer - she literally pays for only about 30% of her groceries, personal products and household supplies. Meaning if her bill is $100 - at the end she pays $30.00. So I asked for a few lessons and am sharing them with you.

First off, perimeter of grocery stores - will normally have manager specials - they are products that they are needing to move and start reducing. Yesterday, I bought a ton of organic products for 75% off. Fresh spinach, herbs, meats and milk! Did you know you can freeze milk........

She can get in and out of her grocery in 5 minutes - because she knows where to look. She may stop on her way to work and on the way home in the same day. And never buys anything other than the specials or what is on her list.

Great sites.... my penny pile - check out the free products. She also gives codes for free Redbox movies on certain days. I thought I was so clever using Redbox until she told me I was paying to much! Ha

Southern savers lists numerous printable coupons, store deals and lists upcoming ads.

Then came dinner - I was going to order a pizza from Donatos and did not have a coupon. She suggested searching Donatos coupons through google. Well I found a coupon for $3.00 off, when i called in the order I provided the code and viola - I saved the money!

Before you purchase anything - search the Internet for deals - you can save money on almost anything!

Stay tuned.......

First off, perimeter of grocery stores - will normally have manager specials - they are products that they are needing to move and start reducing. Yesterday, I bought a ton of organic products for 75% off. Fresh spinach, herbs, meats and milk! Did you know you can freeze milk........

She can get in and out of her grocery in 5 minutes - because she knows where to look. She may stop on her way to work and on the way home in the same day. And never buys anything other than the specials or what is on her list.

Great sites.... my penny pile - check out the free products. She also gives codes for free Redbox movies on certain days. I thought I was so clever using Redbox until she told me I was paying to much! Ha

Southern savers lists numerous printable coupons, store deals and lists upcoming ads.

Then came dinner - I was going to order a pizza from Donatos and did not have a coupon. She suggested searching Donatos coupons through google. Well I found a coupon for $3.00 off, when i called in the order I provided the code and viola - I saved the money!

Before you purchase anything - search the Internet for deals - you can save money on almost anything!

Stay tuned.......

Subscribe to:

Posts (Atom)

{kind=link}

{kind=link}